Recent news reports heralding higher natural gas prices at 19-month highs (Bloomberg) due to cold weather (Reuters) and diminished inventories (even reports of the shale boom ending CSM) piqued my interest. There is hope that natural gas futures are bright (Forth Worth Star Telegram). I wanted to check these narratives against some of my models.

Estimating the marginal utility of money plagues my understanding of economics and greatly affects my ability to model it. However, I developed an alternative deflator called the Energy Price Index (EPI). I took historical Energy Information Agency (EIA) data and performed a regression of the data against the price of oil and natural gas for each fuel source, and then aggregated them based on fraction of total primary energy consumption to get the average price of primary energy delivered to the economy. I tied this model then to the daily WTI crude oil prices and the Henry Hub spot market. Here is an early attempt trying to describe this Economics for Engineers. This model has several problems first it ignores technological change in the conversion of energy to useful work, it assumes that the distribution between energy and non energy feedstocks is fixed, and it uses an adiabatic model of the US economy. The last assumption only affects the estimation of wealth, I perform a more rigorous derivation of the price and money relationships in The Effect of Price in Macroeconomics and have not had time to rebuild my models based on this work. The other two assumptions are a function of my own ignorance. Ayers and Warr estimate the necessary information to fix this error.

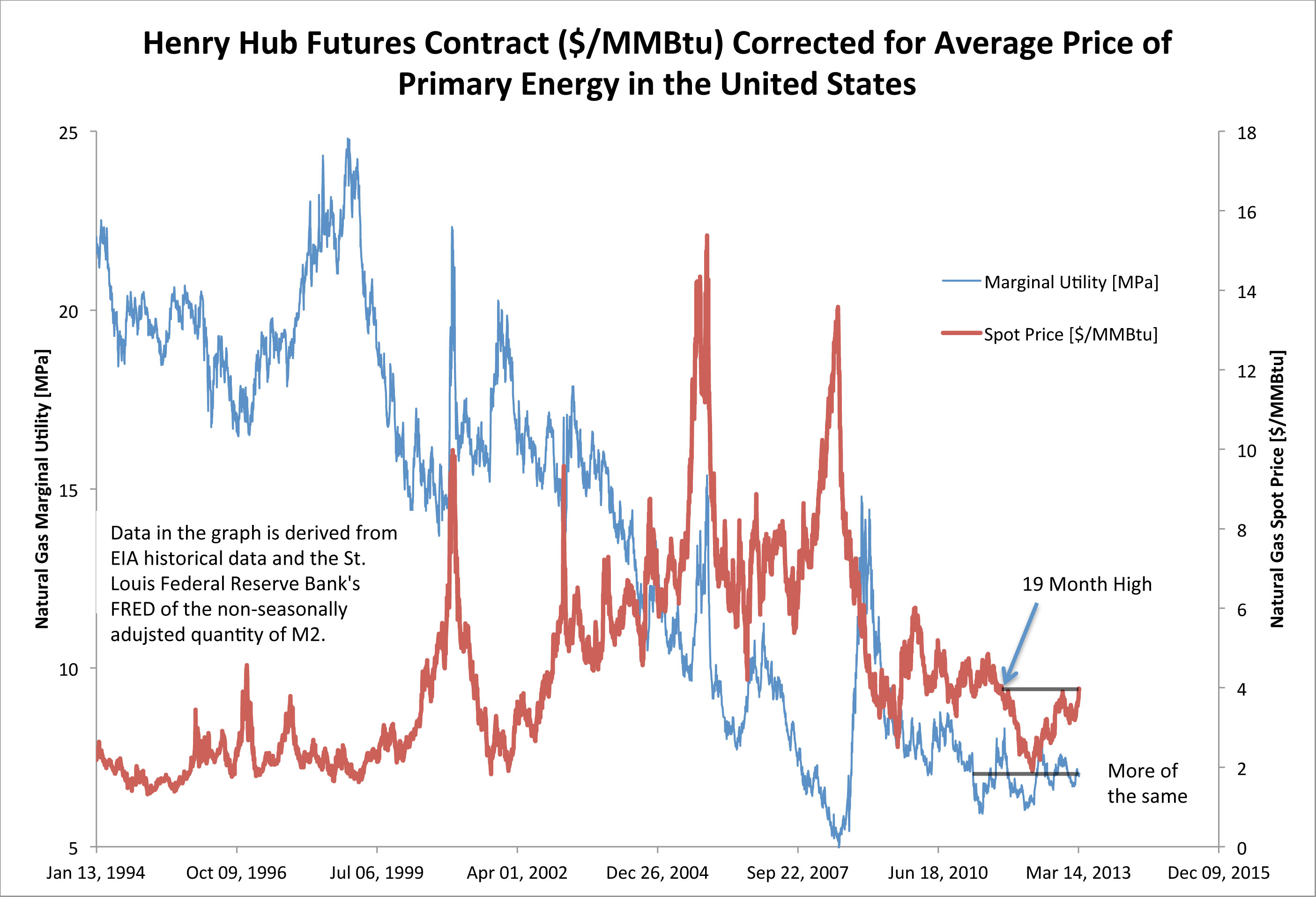

When we look at natural gas prices and compare it with the EPI deflated price, we find some interesting results, Natural Gas Prices.

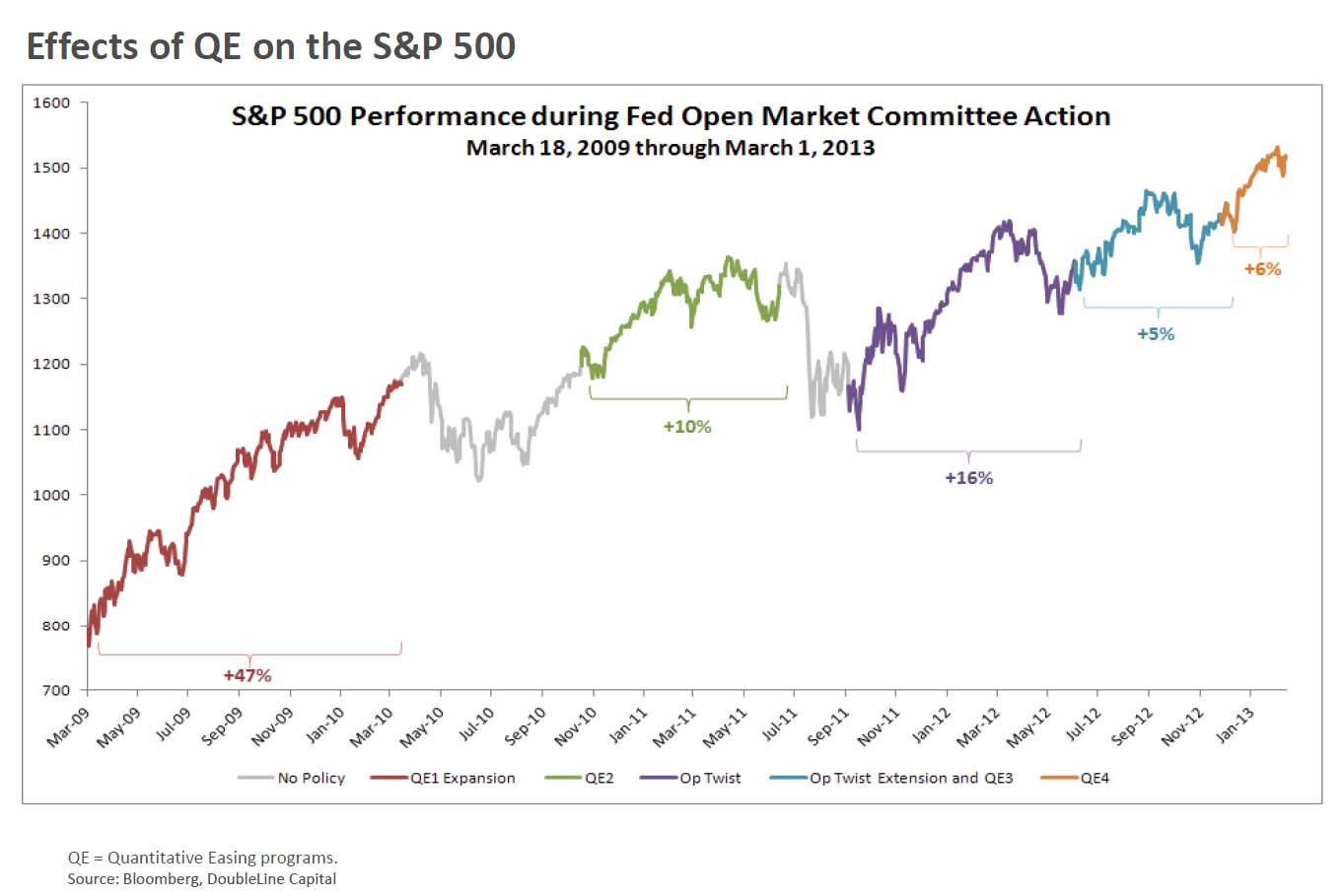

First is that the real price of natural gas is stable and has been this way since roughly first quarter 2010. Second takeaway is that we are starting to see the signs of inflation in energy prices and not just in equities. Here is a graphic from Zero Hedge that shows the impact of Quantitative Easing on the S&P 500. From these two graphs it appears the impacts of inflation were initially noticed on Wall Street and that it appears they are starting to spread into other sectors.

Here is EPI deflated WTI crude oil spot market price graph

Here is the EPI

Here is the EPI

The comparison of the EPI to the CPI shows much more inflation than the CPI. However, the neglect of improvements in the conversion of energy to useful work would have an impact on the EPI moving it closer to parity with the CPI.

{kind=link}

Pingback: Theft at the Grandest Scale « Statistical Economics

Pingback: Quantifying the Value of Bitcoin « Statistical Economics